-

The breadth of strategies targeted by ILS start-ups signals where the industry is heading.

The breadth of strategies targeted by ILS start-ups signals where the industry is heading. -

Demand for top layer coverage may also need to be supported by underlying market growth.

-

As the P&C market shifts, carriers are looking for growth from acquisitions.

-

Competition on price from traditional markets is weighing on bond market momentum.

-

Investor interest is warming up following a colder spell over the past several years.

-

The market has learned lessons from earlier soft market phases that it will apply now.

-

The leadership’s commentary spotlighted to value of ILS to the group.

-

The reinsurer’s capacity is hugely important to ILS firms, with few alternative providers.

-

M&A and shifts in distribution arrangements bring risks and opportunities.

-

The ILS market has won market share at the top of programmes as buying expands.

-

The buzz in the air at ILS Connect told of a market entering its next growth phase.

-

Investor interest and capital flows point to potential for ILS proliferation.

-

Indirect exposure to cat risk through long-term investors gives Markel optionality.

-

Island appetite remains stable, but early 2025 loss activity has injected fresh uncertainty.

-

Several Florida start-ups are poised to begin writing business this year.

-

Wildfire is rarely singled out as an exposure that can shift portfolio outcomes.

-

Management track record has been a factor in capital raising for 2025.

-

Many in the ILS sector are bullish on Milton losses falling at the lower end of earnings impacts.

-

A $40bn Milton loss should barely dent many ILS returns but will trap some capital.

-

Floir approved nearly 650,000 policies for takeout from Citizens for October and November.

-

Winning higher-fee private ILS mandates will strengthen firms’ negotiating positions.

-

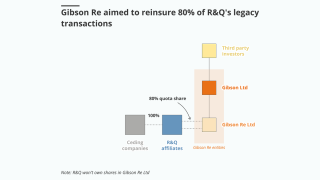

ILS investors’ stress over Gibson Re is unlikely to inhibit legacy ILS’s future.

-

Reinsurer-managers are building out asset management infrastructure as they expand.

-

Relentless focus on annual outcomes provides a packaging that doesn’t fit the purpose.

-

Reinsurers are much better placed to absorb cat losses; insurers are carrying more risk.

-

Top layer competition is an added pressure on ILS firms, but the impact can be overstated.

-

Various trends may work together to hold the cat markets up for longer than some had feared.

-

Pockets of new capital will not shift pricing at mid-year.

-

The depth of the retro market recovery will be an influential factor in the pace of the cat market slowdown from here.

-

Cat bonds and sidecars are well positioned for growth, while private ILS will benefit from further innovations to improve liquidity.

-

Competition for remote risk deals intensified as more capital has targeted the swathe of business that has historically been the heartland of ILS.

-

The cost of maintaining a team to service institutional investors does not always weigh favourably versus bringing in ILS capital.

-

Prior-year cat loss years that are finally shaking out drove fee benefits in Q3.

-

Fermat’s John Seo said the industry can “see the wall of money coming in, but it’s coming in slowly”.

-

A number of players suggested that the cost components of first-party claims were up between 30%-50% on that seen during Ransomware Wave One.

-

A challenge facing the industry in the years to come is the question of how can it move through a rotation of its investor base to capture the growth opportunities that have arisen.

-

The obvious question is where is the capital behind the letters of credit that were being pledged on its transactions.

-

With fundraising still difficult outside the liquid ILS segment, managers are looking for ways to shore up their economic proposition.

-

From seeing ILS as a fleeting competitor to a complement to traditional reinsurance, Denis Kessler’s descriptions of the alternative market were always colourful.

-

Removing any competitor is a positive for ILS peers in a competitive time for fundraising, but it is not clear how much of a boost this will give RenRe.

-

Capital has begun to flow again after a challenging time for ILS fundraising in 2022 – but there is a clear shift underway.

-

There are enough drivers supporting the trend for cat bond segment growth that ILS managers are likely to be plugging this business heavily in the short term, even if it is less attractive in fee yield.

-

The new higher-rate world brings the threat of some investors staying in a risk-off mentality.

-

ILS managers have pioneered externally managed rated carriers, but have done so with cost-consciousness in mind.

-

Reinsurers congregating in Bermuda flagged a lack of interest in helping under-capitalised Floridian insurers and under-priced diversifiers, with positive implications for ILS participation.

-

Fermat’s John Seo divided the potential incoming capital broadly into “fast” and “slow” capital.

-

Should reinsurers retain the option of playing in ILS, or take a ‘go hard or go home’ approach?

-

The outcome over the debate on narrowing cat reinsurance coverage will not be an all-or-nothing bet, with all perils deals with exclusions not a polar opposite of named perils coverage.

-

Several structural factors, including the pricing cycle, make insurers more insulated from US activist states.

-

High-yielding alternatives are taking away attention from this sector, with its complex narrative around recent losses, and diversification only goes so far in selling its story.

-

Announcements and interviews at the UN conference have shed light on the tools emerging to help carriers decarbonise their underwriting portfolios.

-

Major questions confront the industry after Hurricane Ian, but no matter the answers, certain outcomes are inevitable.

-

Buyers are more open than ever to different sources of capacity, but the timing of entry will not be on the industry’s terms.

-

Some are suggesting a rotation of the investor base may be underway, with a move back towards more opportunistic funds.

-

Ratings agencies suggest that carriers must do better on controlling volatility – but diverging risk appetites give the lie to the idea that the industry is walking away from risk.

-

As the ILS market heads back to the office after summer breaks to get stuck into a busy conference season, we recap our top summer features and news coverage that you won’t want to miss.

-

In the absence of a major tactical shift from Demotech, will the reinsurers become the de facto selection party determining which domestics survive?

-

Market orthodoxy suggests cross-class reinsurers secure more leverage – but are there too many implicit offsets in this game?

-

Collaboration should help protect against greenwashing fears but the industry should start with leaving behind the issue of the sector’s “inherent ESG” appeal.

-

With reinsurance availability scarce and costs rising, several carriers have called an interim halt to new homeowners’ business.

-

The carrier has shared insurance and reinsurance risk with ILS partners in the past, but the ILS team reports to Axis Re CEO Steve Arora.

-

In certain areas more collaboration is needed but in others the market will continue to get more diverse as investors respond to post-Irma challenges in differing ways.

-

Even though underlying ILS market conditions are improving, getting a hearing from investors could become harder.

-

Catastrophe reinsurers are already off to a messy start for the year and may have eroded a significant part of their year-to-date Q1 cat budgets as floods are still unfolding in Australia following recent European/UK windstorms.

-

Absent more significant reform, any changes this year look set to simply shift the timing of burdens falling on the public purse.

-

Many investors are in a “hold and assess” pattern on ILS, but some changes in the broader landscape could be more positive for the industry.

-

Greater participation of cat bond investors in the retro market has some advantages alongside the risks.

-

The “squeezed middle” of the reinsurance sector is under pressure, but attritional risk aversion could drive ongoing changes.

-

Cat risk-takers are benefitting from some money leaving the sector, but is this disruption creating inefficiencies as well?

-

This year, instead of talk about running late, people were highlighting how the starting gun has barely been fired.

-

The retro renewals are barely underway, as a challenging fundraising environment and queries over loss experience has delayed the typical pace of progress.

-

Re-allocation of capital rather than true growth seems to be a more likely outcome for the sector in the near term.

-

S&P suggested that an “abrupt rethinking” was a more likely outcome than gradual pricing increases – but a third way is possible if ratings agencies set a glidepath to change.

-

The lower-than-expected losses so far from Ida do not stack up against what is thought to be a $30bn+ cat event.

-

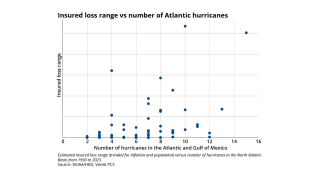

Recently one of my colleagues argued that it was time for a “bonfire of PMLs”, as the past five years have shown that the industry has seriously underpriced the kind of $10bn-$20bn loss events that have been happening since Harvey, Irma and Maria landed in 2017.

-

It is not so much the size of the hit, as the regularity of moderate cat events that is worrying risk-takers.

-

There is no such thing as an average loss year, but investors will still be looking for benchmarks.

-

It’s been a year of high turnover in general, but the ILS low-cost operating model can become a disadvantage in managing through such disruption.

-

Across a wide range of different ILS strategies, there are a number of managers that have failed to gain critical mass in the past 5 years.

-

CPI surged to 4.2% in April, levels not seen since before the Global Financial Crisis.

-

Initially, negotiations are likely to be led by risk takers but there could be a case to model a future role for service providers.

-

The Florida reinsurance renewals ran more smoothly, with lower overall rate increases than initially expected.

-

The latest generation of ILS-backed rated fronting platforms is looking more “ILS-y” due to their ownership structures.

-

Collaboration could address many of the issues vexing the ILS market and help to even out the pace of its recovery.

-

Syndicates and managing agents who want third-party capital support need to deliver on profit and transparency.

-

Could investors – and ILS managers – be ready for another attempt at developing the retail ILS market?

-

Cat bond market exuberance seems to be mismatched against overall ILS sentiment.

-

One swallow doesn't make a summer, but what do two retro "cashback" transactions portend for hurricane season?

-

Last year cat losses were highly dispersed across a large number of events with no single loss above $10bn.

-

A cluster of new launches demonstrate continued interest in an "independent aligned" model.

-

By setting up an asset manager, the reinsurer is competing with ILS firms on their turf.

-

The transaction is a bearish signal for the post-Covid cat reinsurance market.

-

Could a back-to-basics approach see ILS firms shun Lloyd's advantages for lower-cost alternatives?

-

The sting could be in the tail for reinsurers dropping agg risk.

-

Investors from the ILS boom era are also those who've had the least luck, so fundraising remains a slog.

-

Storm Delta may feel like a reprieve, but escaping storms gives no upside for investors.

-

Our ILS Week sessions were packed with thoughtful comments from panellists and fireside chat speakers.

-

Earlier this month, we recapped some of the issues causing rising tensions in the retro market, where providers are pushing for release of capital trapped in connection to Covid-19 claims.

-

Like with Hurricane Irma, the pandemic loss is the kind of disaster that does not highlight the strengths of the collateralised reinsurance and retro model.

-

To what extent does the business opportunity for new start-ups rely on BI losses that the industry is vigorously rebutting?

-

If Covid-19 is a slow-growing loss, fundraising may not come in through fast-access ILS routes.

-

The event could drive greater interest in buying cover for pandemic and contingency risks.

-

The infrastructure of the ILS market is undergoing extensive renovation at the moment.

-

"Access" is one of those magic words or mantras that get horribly over-used in the (re)insurance markets.

-

The January 2020 sidecar renewal season could emerge as a turning point in the evolution of reinsurer ILS tactics and strategies.

-

The topsy-turvy nature of the past few years for the ILS market is apparent when you look at our half-yearly surveys of assets under management.

-

The (re)insurance and ILS industry has headed into a new decade in a spirit of change – as can be seen across multiple lines of business.

-

Every New Year the (re)insurance industry looks back at how much natural disasters cost it in the last 12 months – but the 2019 statistics undercut the value of this exercise.

-

The reinsurance market has scrambled its way through the January renewal season in typical festively messy fashion – but in the sober light of New Year it will be mulling over several key issues that will set the trend for the rest of 2020, with change far from complete.

-

The reinsurance market has scrambled its way through the January renewal season in typical festively messy fashion – but in the sober light of New Year it will be mulling over several key issues that will set the trend for the rest of 2020, with change far from complete.

-

The 2010s are about to end and over the past decade the ILS market has gone through an adolescent growth spurt – heading into 2020 as a far bigger and more complex entity than it was.

-

Most people describing the ILS manager world might break the peer group into three broad categories: reinsurer-affiliated platforms, independent owner-operated firms and asset manager-backed vehicles. Does the market need another category?

-

We have written a bit about how certain (re)insurance business lines, such as retro, are struggling for capacity right now, but another noteworthy development is that some types of structures are also requiring major efforts to shore them up.

-

It used to be called “diworsification” – a phrase coined by Dowling analysts that took hold and became the industry's standard jargon for low-priced international catastrophe risk back around 2011.

-

We've been talking about the reinsurance market being the “squeezed middle” caught in between accelerating primary and retro markets for some time, but could Neon be the first casualty of collateral damage from this phenomenon?

-

The retro renewals are still in the calm-before-the storm phase but it seems that capacity limitations are set to open up more of a role for opportunistic players.

-

Currently, most people trying to describe the ILS manager world might break the peer group into three broad categories: reinsurer-affiliated platforms, independent owner-operated firms and asset manager-backed vehicles.

-

Amid the information overload of results season, “man-made catastrophes” appear to be the main emerging theme – albeit manifesting in two very different ways.

-

Large loss estimate ranges are arguably just masking risk modelling limitations – not improving themBenjamin Franklin apparently once said that ‘nothing in life is certain except death and taxes’ – and it seems like the adage resonated with the risk modellers of the (re)insurance industry.

-

Lloyd's syndicates are hugely reliant on reinsurance and retrocession to manage their catastrophe exposures – so the Corporation's plans to help make it easier for players to source ILS capacity couldn't come soon enough.

-

In the midst of reinsurance conference season you might expect there to be a tendency towards group-think.

-

Cracking into a crème brûlée will always make me think, in passing, of (re)insurance.

-

At Munich Re's ILS roundtable in Monte Carlo, one of the speakers raised the concept of whether a "flight to quality" amongst ILS investors might be better labelled a "flight to alignment".

-

Every year, returning from the Monte Carlo Rendez-Vous is like emerging from a chrysalis – a draining process of freeing oneself from a tiny hive of frantic activity.

-

Rewind a few years and “hot money” was one of the pejorative labels thrown at a burgeoning ILS sector.

-

There’s no doubt that the stress of a serious hit from Hurricane Dorian to Florida reinsurers will add age lines to the ILS market.

-

The reinsurance and ILS markets have spent two years talking about losses, but perhaps more focus on the good years would help reduce some of the noise in the bad years.

-

Do we need new labels for the different types of ILS managers that exist?

-

As ILS reinsurers recover from the 2017-2018 loss years, the consensus view now is that the market will see a “flight to quality” by investors, bolstering the position of some platforms while eroding the asset base of poorer performers.

-

Reinsurers are taking modest rate increases largely by “riding on the backs of primary writers”, Chubb CEO Evan Greenberg said recently.

-

On sweltering weeks like this, you can see why climate change has become a talking point that every ILS manager has to cover in their pitch for new investor mandates.

-

If 2018 is to be a horrible but ultimately beneficial tonic for the overall market, then it is crucial that all players now decide to go above and beyond recommended standards on transparency.

-

Retro brokers are itching to get back to the driver’s wheel – but they may have to wait a bit longerThe retro market has been hard hit in the past couple of years by trapped capital and losses.

-

In a pleasantly warm Zurich this week, I was discussing one of the city’s traditions – burning the giant figure of a snowman to herald the end of winter and coming spring.

-

There has been a fair bit of congratulatory talk about the “discipline” of the (re)insurance market in the past month or so.

-

As the FCA updates the market on its view of the Woodford funds saga, some of the material it is publishing has echoes that may resonate within the ILS market.

-

Timing is everything and, for the reinsurance market, this is especially true when it comes to losses.

-

A move towards more bilateral trades is counter to what you’d expect from a commoditised market.

-

One of my colleagues with an affection for Denis Kessler’s turn of phrase once labelled him the Beyonce of the reinsurance world.

-

Markel has not actually come out and said what it plans to do with former top 10 ILS manager Markel Catco, but the likely money has to be on a gradual closure now that an overwhelming 91 percent of assets under management are due to be returned to investors, as claims development permits.

-

After two years of volatility it’s not surprising to see reports that are urging the ILS market to find more harmonisation and standardisation.

-

Is ILS a sufficient part of Lloyd’s vision for a future of increased efficiency and profitability? There were certainly overtures to alternative capital in the Lloyd’s prospectus launch this week.

-

Perhaps it is not the perfect analogy for an event in Florida, but the famous failure of Devon Loch in the Grand National springs to mind.

-

Earlier this month, Lane Financial speculated that higher Treasury yields would encourage investors to return to the cat bond fold.

-

The relationship between Florida insurers and their reinsurers is obviously going through a rough patch. It makes you wonder whether the role of brokers this year might be akin to that of marriage counsellors.

-

Is this both the best and worst of times for the ILS market?

-

Why has ‘payback’ become a dirty word in the reinsurance markets?

-

What does it say about the insurance market that for every new fund or facility that is launched as a passive or index tracker-style initiative, it seems that another existing one is unwound?

-

Warm winter sun might have helped Miami’s case for bringing ILS folks to the city for one of its annual conferences a couple of weeks ago.

-

The reinsurance industry spends a lot of time obsessing about risk modelling, but arguably its efforts to pin down ever more precise estimates of expected losses are let down by a 20th century approach to data handling.

-

There are some players in our industry who truly believe that any insurance risk can be securitised.

-

Anyone scanning the news stories we have covered in the past week might get a sense of déjà vu.

-

Shipping out risks to ILS partners might lift some weight off insurance balance sheets, but there are other counterweights that are worth bearing in mind.

-

Arguably the single biggest challenge to face reinsurers attempting to attract third-party ILS capital is nothing to do with engaging in fundraising, estimating monthly valuations, or any of the operational facets of asset management.

-

If the ILS market is all about convergence, is it still a worthwhile task to try to create dividing lines within the market, or is a movable border a better representation of messy reality?

-

Regulatory investigations can move at a snail’s pace.

Most Recent